Bitcoin

BlackRock’s BITA Bitcoin ETF Shows Wall Street Is Repackaging Bitcoin for Income Investors

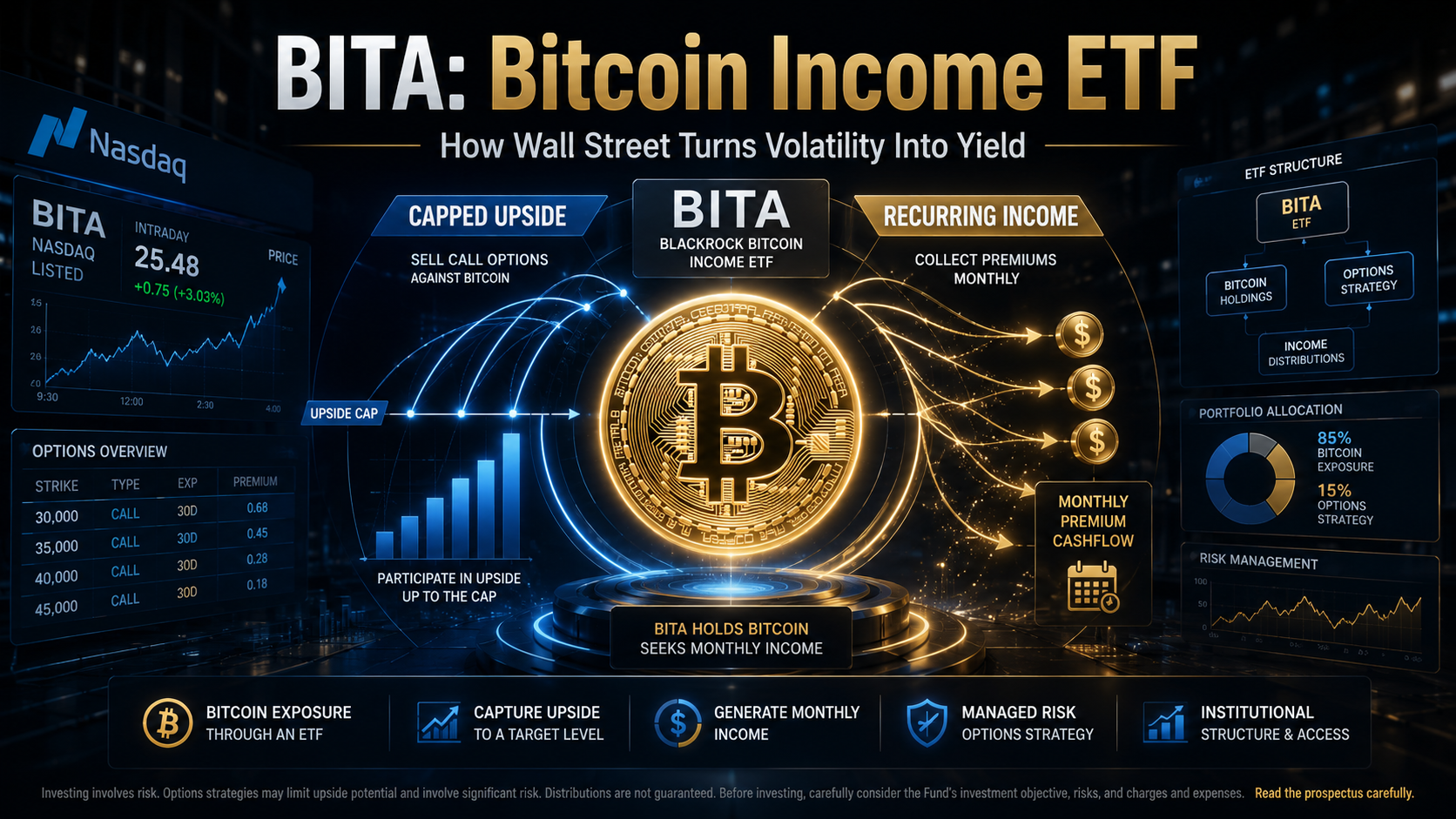

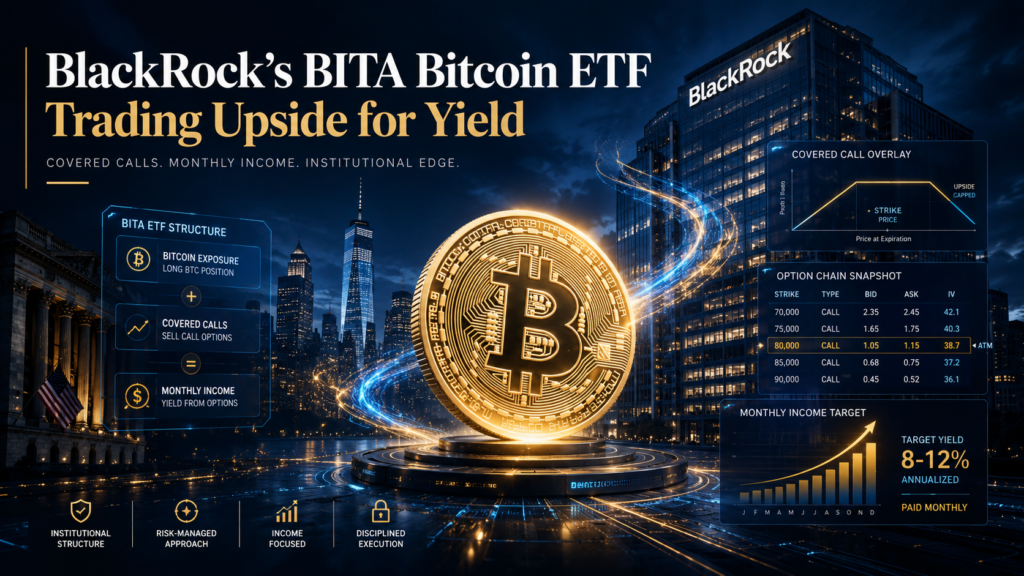

BlackRock’s new iShares Bitcoin Premium Income ETF, trading under the ticker BITA, marks a major shift in how Wall Street is packaging Bitcoin exposure. Instead of offering investors pure participation in Bitcoin’s price movement, BITA combines Bitcoin-linked exposure with an options strategy designed to generate monthly income.

The trade-off is clear. Investors may receive attractive distributions when Bitcoin volatility supports strong option premiums, but they give up part of the upside if Bitcoin rallies sharply. For financial advisors, institutions, and income-focused investors, BITA could make Bitcoin easier to fit into portfolio models. For long-term Bitcoin bulls, however, the structure may feel like a diluted version of direct exposure.

BlackRock Moves Beyond Spot Bitcoin Exposure

BlackRock’s launch of the iShares Bitcoin Premium Income ETF is not simply another crypto ETF listing. It signals the next stage of Bitcoin’s institutional product cycle.

ALSO READ: What They Never Told You About the Security of Cryptocurrencies

The first stage focused on access. Spot Bitcoin ETFs allowed investors to gain exposure to Bitcoin through regulated brokerage accounts without dealing with wallets, private keys, exchanges, or custody risk. BlackRock’s iShares Bitcoin Trust ETF, known as IBIT, quickly became the dominant product in that category.

BITA represents a different objective. It does not only ask whether investors want Bitcoin exposure. It asks whether investors want Bitcoin exposure with monthly income.

That distinction matters because many traditional investors, especially those advised by wealth managers, do not evaluate assets only by price appreciation. They often think in terms of income, volatility, allocation fit, tax treatment, and portfolio behavior. Bitcoin has historically struggled in that conversation because it does not pay dividends, interest, coupons, or staking rewards.

BITA attempts to solve that gap by turning Bitcoin’s volatility into a source of option premium.

How BITA Works

BITA is designed to provide Bitcoin-linked upside while generating monthly distributions through an options overlay.

According to the product structure described by BlackRock, the fund holds a mix of actual Bitcoin exposure and shares of BlackRock’s IBIT. It then sells call options against part of the portfolio, with the options strategy applied to up to 35% of its holdings.

A call option gives the buyer the right to purchase an asset at a set price within a defined period. The seller receives an upfront payment, known as a premium. In BITA’s case, those premiums support the fund’s monthly payout objective.

This structure resembles a covered-call strategy. The fund owns the underlying exposure, then sells calls against a portion of it. If Bitcoin trades sideways, rises moderately, or remains volatile without breaking too far above the option strike prices, the fund can benefit from collected premiums. If Bitcoin surges aggressively, the sold calls can cap part of the upside.

That is the central bargain.

BITA offers income potential in exchange for reduced participation in Bitcoin’s strongest rallies.

Why Bitcoin Volatility Makes This Product Possible

Bitcoin’s volatility often scares conservative investors, but it also makes options more valuable. In options markets, higher expected volatility generally means higher premiums. For a covered-call product, that can create a larger income opportunity.

BlackRock’s head of digital assets, Robert Mitchnick, reportedly described the current payoff profile as roughly 70% upside retention with a mid-to-high-teens yield under current market conditions. That is the kind of structure likely to interest investors who previously viewed Bitcoin as too speculative because it produced no cash flow.

The product does not magically remove Bitcoin risk. It repackages that risk.

BITA still depends on Bitcoin-linked exposure. If Bitcoin falls sharply, option premiums may soften the impact but cannot fully protect investors from losses. The fund’s income stream is also not guaranteed. Monthly distributions depend on market conditions, option premiums, portfolio positioning, fund expenses, and execution.

This is why investors should avoid treating BITA’s projected yield as a fixed-income substitute. It is not a bond. It is a Bitcoin-linked ETF using an options strategy.

Why Financial Advisors May Pay Attention to Bitcoin-linked ETF

BITA may appeal to financial advisors for one practical reason: it creates a more familiar investment conversation around Bitcoin.

Many advisors have clients who are curious about Bitcoin but uncomfortable with pure price exposure. A covered-call-style ETF gives advisors a framework they already understand. They can discuss income, upside cap, volatility harvesting, tax treatment, and allocation sizing. That makes Bitcoin easier to place inside a broader portfolio discussion.

This could be especially relevant for pensions, insurers, family offices, and income-focused investors that have historically avoided Bitcoin because it lacked yield.

The product also gives BlackRock a way to expand beyond IBIT without waiting for a new crypto asset class to gain similar institutional demand. BlackRock already has a leading spot Bitcoin product. BITA lets it segment the Bitcoin market further: pure exposure for growth-oriented investors, premium-income exposure for investors seeking monthly distributions.

That is a classic Wall Street move. Once access is established, product design becomes more targeted.

The Key Trade-Off: Income Today, Less Upside Tomorrow

The most important question for investors is simple: what are they giving up?

A covered-call strategy usually performs best when the underlying asset moves sideways, rises slowly, or remains volatile within a range. It tends to lag during explosive bull markets because part of the upside has been sold away through call options.

That means BITA may suit investors who want moderated Bitcoin exposure and monthly income more than investors who want maximum upside from a major Bitcoin cycle rally.

For example, if Bitcoin enters a strong upward trend, a pure spot Bitcoin ETF may outperform BITA because it does not cap gains through sold calls. If Bitcoin moves sideways while volatility stays elevated, BITA may look more attractive because it can harvest premiums while pure spot exposure produces no income.

This makes BITA less of a direct competitor to IBIT and more of a portfolio-specific alternative.

IBIT is for investors who want clearer Bitcoin beta.

BITA is for investors willing to exchange some upside for monthly income potential.

Why This Launch Matters for the Bitcoin ETF Market

BlackRock’s entry into Bitcoin premium-income ETFs validates a broader trend: crypto ETFs are moving from simple access products toward structured outcome products.

Goldman Sachs filed for a similar Bitcoin income ETF in April, while NEOS already offers the NEOS Bitcoin High Income ETF. This shows that major financial firms see demand for Bitcoin-linked income strategies, especially as investors look for alternatives to traditional yield sources.

The timing is important. Crypto markets have been volatile, and Bitcoin has faced pressure from macro uncertainty, risk-off sentiment, and shifting institutional flows. In that environment, a product that converts volatility into monthly distributions may feel more practical than a pure price-chasing vehicle.

Still, competition will likely grow fast. Once large issuers prove demand, more asset managers may enter with variations: different option coverage levels, different yield targets, different fee structures, and different tax profiles.

That could turn Bitcoin income ETFs into a meaningful subcategory of the digital asset ETF market.

What Investors Should Watch Next

Investors should not judge BITA only by its headline yield. They should monitor several deeper factors.

1. Distribution Consistency

Monthly payouts will matter, but consistency matters more than one impressive annualized yield figure. Investors should watch how distributions behave during low-volatility periods.

2. Upside Capture

The fund’s long-term appeal will depend on how much Bitcoin upside it retains. If Bitcoin rallies and BITA trails too far behind spot ETFs, growth-oriented investors may lose interest.

3. Downside Behavior

Option premiums can reduce some volatility, but they do not provide full downside protection. The fund’s performance during Bitcoin drawdowns will reveal whether income meaningfully offsets losses.

4. Advisor Adoption

If financial advisors begin allocating BITA to client portfolios, the product could become more than a niche ETF. It could become a bridge between Bitcoin exposure and income-focused portfolio construction.

5. Competition From Goldman and Others

Goldman’s filing suggests that more institutional products are coming. Competition may pressure fees, improve product design, and expand investor choice.

The Bigger Picture: Bitcoin Is Becoming Financial Infrastructure

The launch of BITA reflects a deeper institutional shift. Bitcoin is no longer being packaged only as a speculative digital asset. It is being turned into raw material for financial products.

Spot ETFs converted Bitcoin into accessible brokerage-account exposure. Options-based ETFs now convert Bitcoin volatility into income potential. Future products may package Bitcoin into buffer strategies, structured outcomes, retirement models, or institutional allocation tools.

This evolution does not change Bitcoin’s core nature. Bitcoin remains volatile, cyclical, and sensitive to liquidity, macro conditions, regulation, and investor sentiment. But it does change how traditional finance interacts with it.

Wall Street is no longer asking whether Bitcoin belongs in markets. It is asking how many different products can be built around it.

Final Analysis

BlackRock’s BITA ETF is important because it shows how the Bitcoin ETF market is maturing. The product is not designed for investors who want full exposure to every Bitcoin rally. It is built for investors who want a more structured way to participate in Bitcoin while receiving monthly income potential.

That makes BITA both useful and limited.

Its strength is its ability to make Bitcoin more accessible to income-focused investors, financial advisors, and institutions that need a clearer portfolio rationale. Its weakness is the same trade-off that defines all covered-call strategies: the income comes at the cost of capped upside.

For investors, the decision should start with objective, not yield.

Those seeking maximum long-term Bitcoin appreciation may prefer direct Bitcoin exposure or a spot Bitcoin ETF. Those seeking partial Bitcoin participation with monthly distributions may find BITA more aligned with their needs.

The product does not make Bitcoin conservative. It makes Bitcoin more programmable inside traditional portfolio structures.

That may be the real story. BlackRock is not only selling another Bitcoin ETF. It is helping turn Bitcoin volatility into a Wall Street income product.

FAQs

What is BlackRock’s BITA ETF?

BITA is the iShares Bitcoin Premium Income ETF. It provides Bitcoin-linked exposure while using an options strategy to generate monthly premium income.

How does BITA generate income?

BITA sells call options against part of its Bitcoin-linked holdings. The fund collects option premiums, which support monthly distributions.

Does BITA offer full Bitcoin upside?

No. BITA offers partial Bitcoin upside because its call-option strategy can cap gains if Bitcoin rises sharply.

Is BITA the same as IBIT?

No. IBIT is BlackRock’s spot Bitcoin ETF designed to reflect Bitcoin’s price performance. BITA combines Bitcoin-linked exposure with an income-generating options strategy.

Is BITA suitable for all investors?

No. BITA carries Bitcoin-related market risk and options-strategy risk. It may suit investors seeking income-oriented Bitcoin exposure, but investors should review the fund’s prospectus, risk disclosures, fees, and tax treatment before making any decision.

Disclaimer: This article is for informational and educational purposes only. It does not provide financial, investment, legal, or tax advice. Cryptocurrency and ETF investments involve risk, including possible loss of principal.

The myths, the misconceptions, and the uncomfortable truths about cryptocurrencies, payments, exchanges, and your savings.

The cryptocurrency industry built its brand on three promises. Unhackable. Anonymous. The safest place for your money.

Each promise contains a grain of truth wrapped in a thick layer of marketing. Scratch the surface and a different picture appears. The technology is strong. The systems around it are fragile. The people using it carry most of the risk.

This article separates the myths of cryptocurrencies from the realities. It answers two questions that millions of investors ask and few get answered honestly. Are crypto payments really secure and encrypted? And can you trust centralized or decentralized exchanges with your savings?

The short answers are simple. Crypto payments are secured by cryptography, but they are not encrypted, private, or anonymous in the way most people imagine. And no exchange, centralized or decentralized, should ever be treated as a savings account. The long answers are where your money gets saved or lost.

The Word “Crypto” Fooled Everyone

Start with the name itself. The “crypto” in cryptocurrency refers to cryptography, not encryption. The two terms sound similar. They do very different jobs.

Encryption hides data. It scrambles a message so only the intended reader can see it. Your WhatsApp chats and your online banking sessions work this way.

Cryptography on a public blockchain does something else. It proves things. It proves that a transaction is valid. It proves that the rightful owner authorized a payment. It proves that nobody tampered with the record. It hides nothing.

This single misunderstanding sits at the root of almost every crypto security myth. Once you see the difference, the rest of the picture falls into place.

Myth 1: Crypto Payments Are Encrypted and Hidden

The myth: Every crypto payment travels inside a sealed envelope that nobody can open.

The reality: Bitcoin, Ethereum, Solana, and almost every major public blockchain are transparent ledgers. Every transaction, every wallet address, and every balance sits in public view. Anyone with an internet connection and a block explorer can inspect them, forever.

The network does not need to hide a transaction to secure it. It needs to prove the transaction is valid. Three cryptographic tools do that work.

| Cryptographic tool | What it does | What it does not do |

| Hashing | Links blocks together and makes tampering visible | Does not hide transaction data |

| Digital signatures | Prove the owner authorized the payment | Do not hide sender, receiver, or amount |

| Merkle trees | Let anyone verify a transaction belongs in a block | Do not make payments private |

Here is a detail almost nobody mentions. For most of Bitcoin’s history, even the network traffic between nodes traveled as plain, unencrypted text. Encrypted peer-to-peer transport only arrived with an upgrade known as BIP 324, and it protects communication between nodes. It does not encrypt the ledger itself. The “encrypted payments” myth was wrong at every layer.

The accurate sentence reads like this. Cryptocurrencies are cryptographically secured, publicly visible, and permanently recorded.

Myth 2: Crypto Is Anonymous

The myth: Nobody can tell who sent or received a crypto payment.

The reality: Public blockchains are pseudonymous, not anonymous. Your wallet address does not display your passport name. But every transaction that address ever made is public, and the trail never goes cold.

The pseudonymity is thinner than most users believe. Blockchain analytics firms such as Chainalysis and TRM Labs exist for exactly this reason. They cluster addresses, label exchange wallets, map sanctioned entities, and trace flows across chains. Law enforcement has recovered funds and identified suspects years after the original transactions.

The weak point is the moment of connection. The instant your address touches an exchange that verified your identity, a merchant, a bridge, or even a careless social media post, your name links to your entire on-chain history. Past and future.

This leads to an uncomfortable conclusion. For privacy, Bitcoin can be worse than a bank account. Your bank statement stays private between you, your bank, and authorized regulators. Your Bitcoin address history can be read by anyone on earth, forever.

The Privacy Coin Exception

A small category of crypto networks genuinely conceals transaction data. They are the exception that proves the rule.

Monero uses ring signatures and stealth addresses to obscure who signed a transaction and who received it. Zcash uses a system called zk-SNARKs to support shielded transactions, which prove a payment is valid without revealing the details underneath.

Even here, precision matters. These networks do not simply “encrypt payments” in the everyday sense. They use privacy-preserving cryptographic systems that obscure the sender, the receiver, the amount, or the links between transactions, depending on the network and the transaction type.

That privacy comes at a price. Regulators dislike what they cannot trace. Many exchanges have delisted or restricted privacy coins under compliance pressure. If you hold them, expect fewer doors to be open.

Myth 3: A Secure Blockchain Means Your Funds Are Secure

This is where most people actually lose money.

Bitcoin has never been hacked at the protocol level. Ethereum’s core protocol has proven equally robust. A successful attack on Bitcoin’s consensus would require billions of dollars in hardware and energy, and it would buy only a temporary, highly visible disruption. Smaller chains tell a different story. Networks with thin mining power, including Ethereum Classic and Bitcoin Gold, have suffered successful 51 percent attacks. Security scales with the economic weight behind a chain. It is not an automatic property of the word “blockchain.”

But here is the brutal part. The protocol is almost never the weak point. The attack surface sits around it, and it points directly at you.

| Attack surface | How it works |

| Phishing | Fake wallet popups and cloned exchange login pages capture your credentials |

| Malware | Clipboard hijackers silently swap the wallet address you copied |

| SIM swaps | Attackers take over your phone number and reset your accounts |

| Fake apps | Malicious wallet and exchange apps drain funds on first use |

| Seed phrase theft | Fake support agents trick users into typing recovery phrases |

| Blind signing | Users approve transactions they cannot read or understand |

| Address poisoning | Tiny transfers from lookalike addresses bait a copy-paste mistake |

The blockchain behaves perfectly while the user signs a malicious transaction. And once that transaction confirms, it is final. No chargeback. No fraud department. No customer service line. Irreversibility is a feature of the system and a catastrophe for the careless.

The honest summary stings. A system can be technically secure and still unsafe for ordinary users.

Centralized Exchanges: The Convenient Illusion

Centralized exchanges, known as CEXs, act like brokerages. Platforms such as Coinbase, Binance, and Kraken hold your crypto for you, match your trades, and control the private keys on your behalf. That convenience reintroduces the exact risk crypto was designed to remove. You must trust a company.

Myth 4: An Exchange Balance Is Like a Bank Balance

It is not, and the difference is legal, not technical.

A bank deposit in most developed markets carries government insurance up to defined limits, such as FDIC coverage in the United States or FSCS protection in the United Kingdom. If the bank fails, you get your cash back.

A crypto exchange balance carries no such guarantee. When you hold coins on an exchange, you do not hold the asset. You hold a claim against the exchange’s internal ledger. If the exchange fails, you become an unsecured creditor standing in a bankruptcy line.

History has run this experiment twice at scale. FTX collapsed in 2022 after customer money was misused, and its founder Sam Bankman-Fried was sentenced to 25 years in prison. Mt. Gox failed earlier, and its creditors waited roughly a decade before repayments finally began in 2024.

One nuance deserves attention because marketing teams exploit it. Some platforms hold customer fiat balances in pass-through accounts that carry deposit insurance. People hear the word “insured” and assume their Bitcoin is covered. It is not. Only the dollars are, and only in specific custodial arrangements. Read the fine print before you believe the badge.

Myth 5: Regulated Means Safe

Regulation helps. It does not make an exchange hack-proof or failure-proof, and “regulated” is not one universal standard.

The questions that matter are specific. Regulated where, and by whom? Are client assets segregated from company funds? Are liabilities audited, not just assets? Is custody independent? Strong regimes answer these questions with rules. Dubai’s VARA custody framework requires client virtual assets to sit in segregated wallets and prohibits the rehypothecation of assets held in custody. The EU’s MiCA framework imposes authorization, supervision, transparency, and investor-protection requirements on crypto service providers, and European regulators have warned firms against misleading customers about which services those protections actually cover.

An exchange under VARA or MiCA operates on a different planet from an offshore entity with no defined regulator. But even the best regime only reduces risk. It never removes it.

Myth 6: Proof of Reserves Proves Solvency

After FTX, proof of reserves became the industry’s favorite trust signal. It is half a balance sheet.

Proof of reserves shows that an exchange controlled certain wallet balances at a single point in time. Solvency requires both sides of the ledger. Assets minus liabilities equals the truth. An exchange can publish impressive reserves while hiding loans, off-chain obligations, related-party exposure, or assets borrowed just for the snapshot.

The US Securities and Exchange Commission warned investors to treat proof of reserves reports with extreme caution, noting that they do not provide the protections of a financial statement audit and may not prove an exchange can meet its customer liabilities.

The correct reading is narrow. Proof of reserves beats no proof. It is not an audit, and it is not a guarantee.

Myth 7: Cold Storage Makes an Exchange Unhackable

The Bybit incident destroyed this idea.

In February 2025, attackers stole roughly 1.5 billion dollars from Bybit in the largest crypto heist on record. The funds came from an Ethereum cold wallet. The attackers did not crack the vault. They compromised the transaction approval process and changed what Bybit’s own signers saw on their screens, so trusted humans authorized the malicious transfer themselves.

The lesson reaches beyond one exchange. Cold storage protects keys from constant internet exposure. It does not protect against a poisoned signing workflow, a compromised interface, or a manipulated approval chain. Security is not only about where the keys sit. It is about how transactions get created, reviewed, signed, and stopped.

The scale of the problem is measurable. Chainalysis reported around 2.2 billion dollars stolen from crypto platforms in 2024. TRM Labs reported that illicit actors stole 2.87 billion dollars across nearly 150 hacks in 2025, with Bybit accounting for a major share of the total.

The CEX Verdict

Use a strong, well-regulated exchange for what it does well. Buying crypto with fiat. Selling back into fiat. Active trading. Short-term liquidity.

Never use it as a long-term vault, a substitute for a bank, or a home for money you cannot afford to lose. The rule fits in one line. Use exchanges for access and execution. Do not confuse access with custody.

Decentralized Exchanges: Different Risk, Not Less Risk

Decentralized exchanges, known as DEXs, flip the custody model. Platforms such as Uniswap and PancakeSwap let you trade directly from your own wallet through automated smart contracts. No company holds your funds. The old saying applies. Not your keys, not your coins. On a DEX, the keys stay yours.

That removes corporate failure risk. It does not remove risk. It transfers risk to the code and to you.

Myth 8: No Middleman Means Nothing Can Collapse

A DEX cannot go bankrupt like a company. But it lives entirely inside code, and code carries its own failure modes. Billions of dollars have been drained through smart contract exploits, and the categories repeat. Reentrancy bugs that let attackers loop withdrawals. Oracle manipulation that distorts the prices a protocol relies on. Flash loan attacks that borrow enormous sums, twist a market, and repay the loan inside a single atomic transaction. And admin key compromises, where a supposedly decentralized protocol turns out to have an upgrade key controlled by one person or one small team.

DeFi does not remove risk. It changes who carries it.

Myth 9: Audited Means Safe

An audit is a professional review of known code at a fixed point in time. It is not a guarantee.

Audits routinely miss economic exploits, governance attacks, bad upgrade logic, bridge weaknesses, and bugs introduced after the audit shipped. Many DeFi disasters involve contracts that work exactly as coded while the economic assumptions behind them break. Plenty of audited protocols have been drained.

The better question is never “was it audited.” The better question is what was audited, by whom, when, after which code changes, and against which economic assumptions.

Myth 10: Token Approvals Are Harmless

Approvals are the most underestimated risk in DeFi, and the danger is delayed.

When you trade on a DEX or use a lending app, you grant a smart contract permission to spend tokens from your wallet. Many apps request unlimited approval because it smooths the user experience. That permission does not expire when your trade finishes. The contract keeps it.

You can interact with a protocol today and lose funds months later, after you forgot the interaction entirely, if that contract, its front end, or its admin keys become compromised. Basic hygiene fixes most of this.

- Avoid unlimited approvals whenever possible

- Grant limited approvals for specific trades

- Revoke stale approvals on a regular schedule

- Keep separate wallets for savings and for DeFi activity

- Never connect your cold-storage wallet to random apps

Myth 11: A Safe Contract Means a Safe Website

The website is a separate attack surface. A DEX can run flawless contracts while the front end you visit serves you poison.

Attackers hijack DNS records, clone official sites, inject malicious code into pages, and manipulate the transaction details that appear in your wallet. Several major protocols have suffered exactly this kind of front-end compromise while their contracts remained untouched.

Experienced users verify contract addresses, bookmark official sites, and read every detail on a hardware wallet screen before signing. The few seconds of friction are the price of survival.

One more quiet cost deserves a mention. Bots monitor pending transactions in the public mempool, jump ahead of your trade, and extract value through slippage in what traders call sandwich attacks. This is not theft in the legal sense. It is a tax on inattention, charged on every careless trade.

Myth 12: DEX Yield Is Like Bank Interest

Providing liquidity to a DEX pool is market making, not saving.

You earn fees, and in exchange you accept smart contract risk, token collapse risk, pool imbalance, and a phenomenon called impermanent loss, where price movements leave you with less value than if you had simply held the tokens. A bank pays interest inside a regulated lending framework. A DEX pool pays yield because you supplied capital into a volatile automated market.

The honest sentence reads like this. DEX yield is compensation for risk, not guaranteed interest.

Myth 13: Stablecoins Are Safe Savings

Stablecoins remove most price volatility. They do not remove risk. They concentrate it in the issuer.

A dollar-backed stablecoin can hold its peg for years and still fail under reserve pressure, legal action, or a redemption rush. Holders also face freeze risk, since major issuers can lock addresses, plus smart contract risk and jurisdiction risk on top.

Stablecoins are excellent payment and settlement instruments. They are not insured deposits, and treating them as one confuses a tool with a vault.

The Distinction That Saves Portfolios: Payment Security vs Savings Safety

These two questions get blended together constantly, and the blending costs people money. A payment network can be secure while being a terrible place for savings.

Bitcoin settles transactions securely while its price can fall sharply. Ethereum executes contracts flawlessly while a user signs a malicious approval. A CEX processes trades smoothly while sliding toward insolvency. A DEX avoids custody risk while exposing you to code risk. A stablecoin holds its peg while its issuer faces a regulator.

Security is not one thing. It has layers, and each layer asks its own question.

| Security layer | The question it answers |

| Protocol security | Can the chain be rewritten, forged, or double-spent? |

| Wallet security | Can someone steal your keys or trick you into signing? |

| Exchange security | Can the custodian protect assets and stay solvent? |

| Smart contract security | Can the code be exploited? |

| Privacy | Can others link your transactions to you? |

| Legal protection | Do you have enforceable rights when things go wrong? |

| Market risk | Can the asset collapse in price? |

| Operational recovery | Is there any way back after a mistake? |

Most crypto losses happen because users obsess over one layer and ignore the other seven.

So Where Should Your Savings Actually Live?

If you treat crypto as a long-term savings vehicle, neither a CEX nor a DEX is the answer. The strongest position for long-term holdings is self-custody through a hardware wallet, a physical device that keeps your private keys offline and isolated from the internet.

But self-custody is not magic. It is risk transferred, not risk removed. You shed exchange bankruptcy risk and most remote hacking risk. In exchange, you inherit a new list. Seed phrase loss, with no recovery path in existence. Supply chain attacks, which is why you buy devices only from the manufacturer. Blind signing risk when a hardware wallet touches DeFi. Physical coercion. Fire, flood, and theft. And the inheritance problem, because if you die without a succession plan, the funds are gone permanently.

For small amounts, a reputable hardware wallet with a carefully stored seed backup may be enough. For serious money, the bar rises. Multisig setups that require multiple keys to move funds. Passphrase-protected wallets. Geographically distributed, fireproof backups. Written recovery procedures. Clear inheritance instructions. For institutional-size holdings, regulated qualified custodians enter the picture.

The right philosophy fits in one sentence. Self-custody is responsibility converted into infrastructure.

A Practical Three-Bucket Model

Divide your crypto into three buckets and never let them share a wallet.

| Bucket | Where it belongs | Purpose |

| Daily trading funds | Reputable, well-regulated CEX | Active trades, fiat conversion, quick liquidity |

| DeFi experiment funds | Separate hot wallet | DEX swaps, staking, testing, airdrops |

| Long-term savings | Hardware wallet, multisig, or qualified custody | Capital protection and long-term holding |

The wallet that signs DeFi approvals must never be the wallet that holds your savings. One compromised approval should cost you an experiment, not a future.

The Final Verdict

Crypto payments are secure in one narrow but important sense. Major public blockchains use cryptography to prevent unauthorized spending, counterfeiting, and tampering, and they do that job extraordinarily well. But those payments are not encrypted, not private, and not anonymous. They are transparent records that anyone can read, forever.

Centralized exchanges are gateways and trading venues. They reintroduce the counterparty risk that crypto was built to eliminate, and history shows what happens when that risk matures. Decentralized exchanges remove the counterparty and hand you the technical risk instead, wrapped in code you probably never read.

Neither one is a savings account. Savings belong in disciplined self-custody, behind hardware, backups, and written procedures. The price of that sovereignty is total personal responsibility, and nobody collects that price more reliably than the crypto market.

The technology never lied to you. The marketing did. Now you know the difference.

FAQs

Are crypto payments encrypted?

Most crypto payments are cryptographically secured, but they are not encrypted in the way many people assume. Public blockchains such as Bitcoin and Ethereum record transactions on transparent ledgers where wallet addresses, transaction amounts, and balances can usually be inspected by anyone.

Is cryptocurrency anonymous?

Most cryptocurrencies are pseudonymous rather than anonymous. A wallet address does not automatically show a user’s real name, but blockchain analytics tools can often trace activity and link addresses to exchanges, merchants, bridges, or other identity points.

Are centralized crypto exchanges safe for savings?

Centralized exchanges can be useful for buying, selling, and trading crypto, but they should not be treated like savings accounts. Exchange balances carry counterparty risk, bankruptcy risk, custody risk, and limited legal protection compared with insured bank deposits.

What is the difference between a CEX and a DEX?

A centralized exchange, or CEX, holds user assets and manages trades through its own platform. A decentralized exchange, or DEX, lets users trade from their own wallets through smart contracts. CEXs create company and custody risk, while DEXs create smart contract, approval, front-end, and user-error risk.

Does proof of reserves prove that an exchange is safe?

Proof of reserves can show that an exchange controlled certain assets at a specific time, but it does not prove full solvency. A complete picture also requires liabilities, off-chain obligations, loans, related-party exposure, and independent financial audits.

Are hardware wallets the safest way to store crypto?

Hardware wallets are one of the strongest options for long-term crypto storage because they keep private keys offline. However, they still require careful seed phrase storage, backup planning, inheritance instructions, and protection against physical loss, theft, or blind signing.

What is the safest way to manage crypto holdings?

A practical approach is to separate crypto into three buckets: trading funds on a reputable exchange, DeFi funds in a separate hot wallet, and long-term holdings in a hardware wallet, multisig setup, or qualified custody solution. This limits the damage if one wallet, platform, or approval is compromised.

Disclaimer: This article is for informational and educational purposes only. It does not provide financial, investment, legal, or tax advice. Cryptocurrency and ETF investments involve risk, including possible loss of principal.

What They Never Told You About the Security of Cryptocurrencies

BlackRock’s BITA Bitcoin ETF Shows Wall Street Is Repackaging Bitcoin for Income Investors

BlackRock’s BITA Bitcoin ETF Shows Wall Street Is Repackaging Bitcoin for Income Investors

Pingback: What They Never Told You About the Security of Cryptocurrencies - The Crypto Encounter